How to Hedge Inflation and Avoid the Biggest Bond Risk

Bonds are less volatile than stocks – but in the long-term they’re just as risky. This post examines the best ways to hedge inflation risk.

There’s a big difference between volatility and risk. Volatility is the magnitude of short-term price changes. Risk is the potential of permanently losing money.

“Uncertainty is not the same as risk. Indeed, when great uncertainty drives securities prices to especially low levels, they often become less risky investments.”Seth Klarman

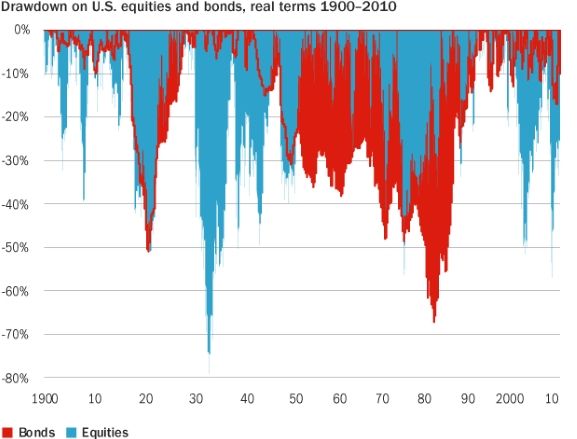

Bonds are less volatile than stocks – but in the long-term they’re just as risky. Long-term US Treasury bond investors lost 60% in inflation-adjusted terms from 1940 to 1981.

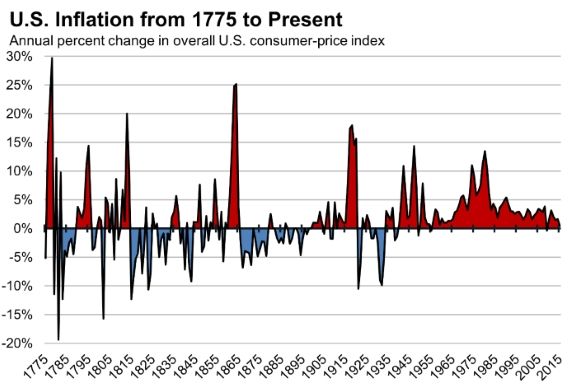

Inflation is the biggest long-term risk for bond investors. A 10-year Treasury bond yielding 7% in 1976 might have seemed like a fair rate at the time – but annual inflation accelerated to 15% by 1981, completely eroding the yield’s true value.

Treasury inflation-protected securities (TIPS) are not exposed to this risk since their principal and interest are adjusted higher with inflation. US TIPS were first issued in 1997 and are still thought of as the new kid on the bond block. The nature of TIPS cash flows make them more similar to bonds of 100 years ago than the regular Treasuries we think of as the “original” bonds.

Inflation behaved differently before countries abandoned the gold standard. Inflation was volatile, but not persistent.

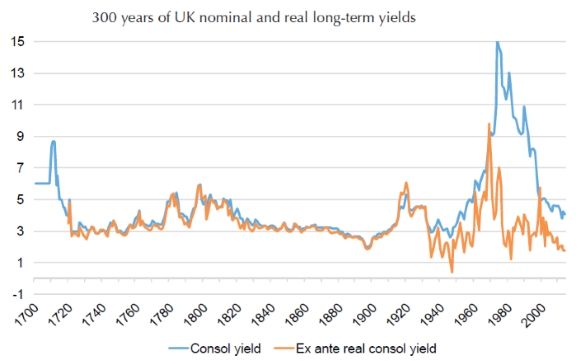

A lack of long-term inflation meant a bond investor in the 1800s was confident $1 in the present would buy the same amount of goods in the future. Pre-inflation government bond yields were essentially the same as after-inflation yields.

The disappearance of the gold standard resulted in a “thousand year flood” for bond investors.

Inflation Hedges

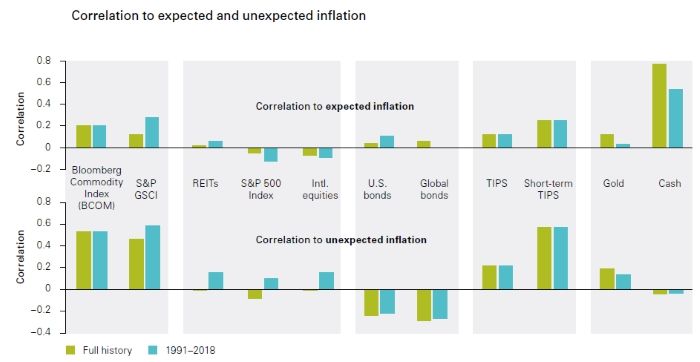

The chart below shows the correlation of major asset classes to inflation.

Investors should care more about correlation to unexpected inflation – expected inflation is already baked into current market prices.

All TIPS receive the same inflation adjustment, so you might wonder why short-term TIPS exhibit a higher correlation. Short-term TIPS have a lower duration than long-term TIPS and are less sensitive to changes in real yields. This means inflation-indexed income payments make up a larger portion of the investment’s total return. Additionally, long-term TIPS have more to do with inflation experienced over the entire life of the bond – not an immediate inflation shock.

TIPS don’t offer a perfect 1.0 correlation to inflation since TIPS prices move inversely to real yields in the short-term. It’s important to not get caught up in correlation minutiae – TIPS held to maturity guarantee a real return regardless of the path they take along the way.

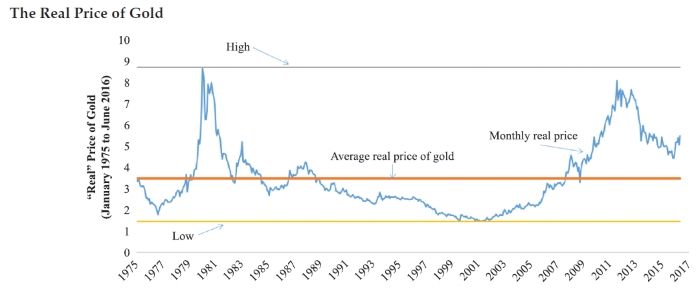

Gold is not an effective inflation hedge for time horizons that matter. The inflation-adjusted price of gold has fallen for extended stretches of time. If gold closely tracked inflation its inflation-adjusted price would be a horizontal line.

It’s true that gold investors do have (extremely) long-term data on their side. The annual pay of a U.S. Army private, in ounces of gold, is roughly equal to how much a Roman soldier earned in gold. That said, it doesn’t help an investor if their gold allocation trailed inflation during their lifetime only to gain it back thirty years later.

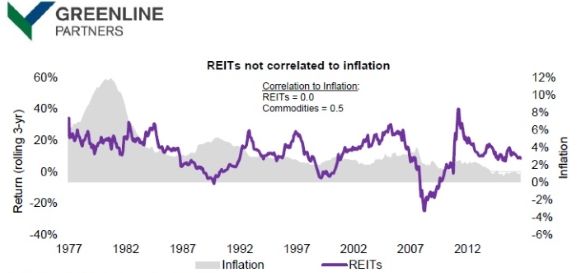

Stocks and REITs are not effective short-term inflation hedges. Both stocks and REITS have outperformed inflation over extended periods of time – but this doesn’t mean they’re inflation hedges. Companies can eventually pass on higher costs and REITs can eventually raise rents. Your inflation adjustment will come, but it might be years after inflation takes off.

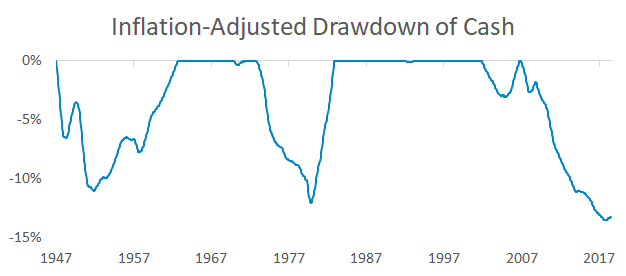

Cash is not an inflation hedge. There have been multiple 10+ year periods where Treasury bills have failed to outpace inflation. The ability of cash to hedge inflation is a function of how benevolent central bankers are in giving savers a fair rate.

Based on the post-crisis experience, I wouldn’t be comfortable betting on cash to provide investors with a real return in the future.

Summary

- Regular bonds are risky in the long-term since they’re vulnerable to inflation.

- The inflation-protected cash flows of TIPS make them similar to bonds before the era of persistent inflation.

- TIPS have historically exhibited a high positive correlation to unexpected inflation.

This is the second in a 5-part series on TIPS. Here are links to the other posts: