Small Portfolio Changes Don’t Matter

This post examines the (shockingly small) total portfolio impact of small investment allocations.

The investment product landscape is like the supplement industry. Supplement companies don’t make money if you sleep eight hours a night, only drink water, and avoid junk food. Fund providers don’t make money if you stick to low-cost index funds. We’re inundated with products promising an edge, either for our health or finances. In investing, these products are typically marketed as satellite allocations to complement a core portfolio.

This post examines the total portfolio impact of small allocations. All hypothetical portfolios shown are annually rebalanced and include reinvested dividends and interest. I used Portfolio Visualizer for all of the below analysis.

Smart Beta

Smart beta funds imply that a portfolio advantage is one mouse-click away. Investors have bought into the marketing – Vanguard’s Value ETF (VTV) has $45 billion in assets. Like a placebo, owning VTV only feels like you’re doing something since the fund’s performance is identical to the broad U.S. stock market. Other smart beta products like low volatility and quality stock funds have attracted billions in inflows. Some of these funds are closet indexers like VTV, but some are truly different and provide concentrated exposure.

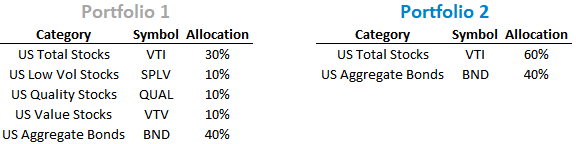

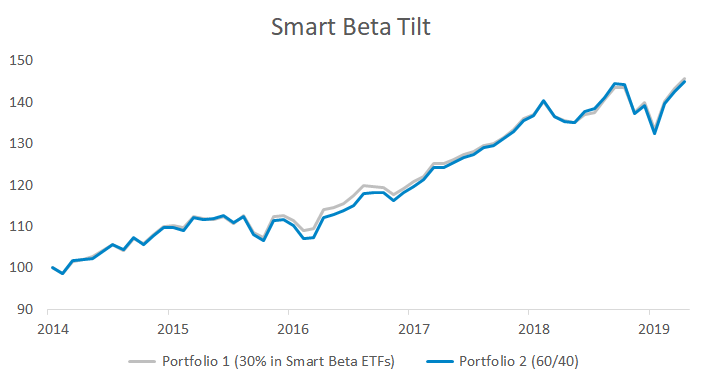

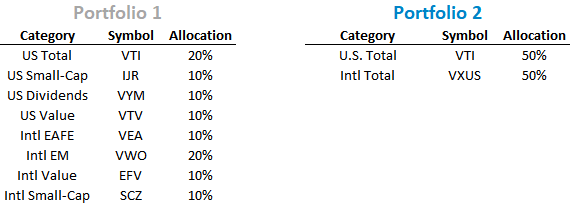

Since smart beta funds are typically implemented as satellite allocations, investors should care if these small tilts actually impact performance. The table and graph below show two portfolios. One has half of its 60% stock exposure in smart beta funds. The other is a 60/40 portfolio with 60% in Vanguard’s total market-cap stock fund and 40% in Vanguard’s aggregate bond fund.

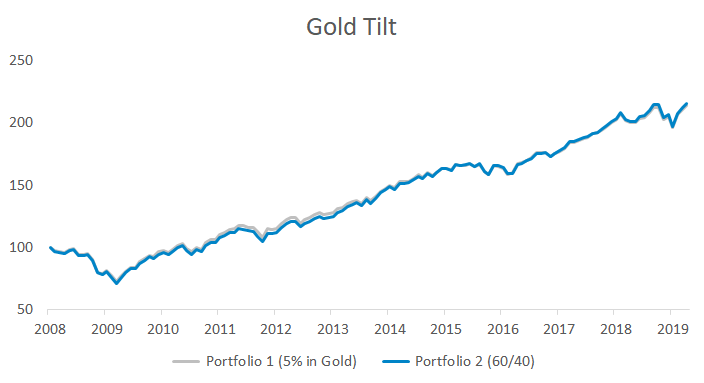

Gold

Gold (and commodities in general) are popular with investors concerned over inflation or political risk. I’m not trying to debate the investment merit of gold – what I do take issue with is the common prescription of a 5% allocation.

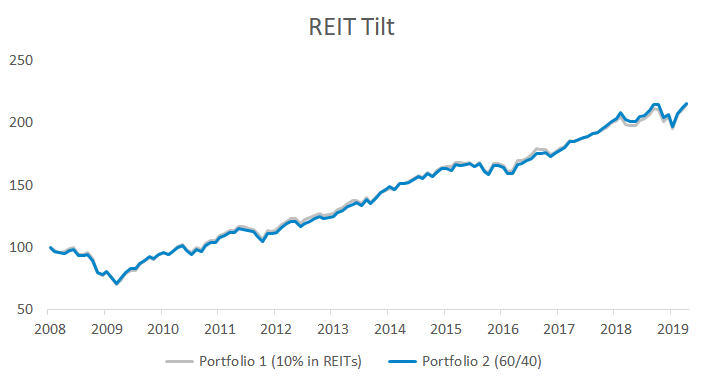

REITs

Real estate investment trusts tout stock-like returns, high dividends, and low correlation to stocks. Let’s say an investor carved out 10% of their equity exposure and allocated it to REITs. Would it have made a difference over the past decade?

Stock Slice-and-Dice

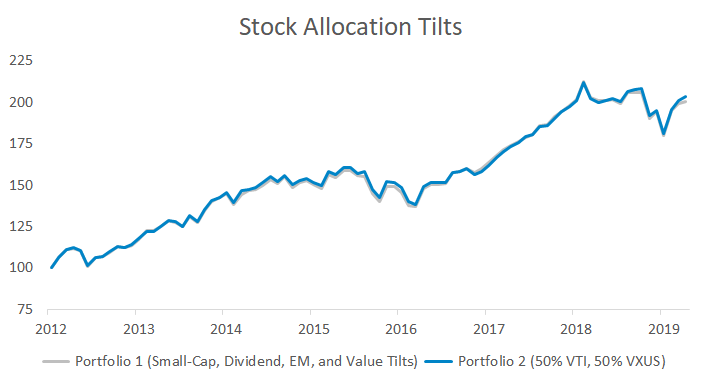

Slice-and-dice portfolios try to outperform the broad market by overweighting market segments that have historically outperformed. Let’s say an investor decided to overweight small-cap, dividend, and value stocks. Has this made a difference compared to a 50/50 split between Vanguard’s total market-cap domestic and international funds?

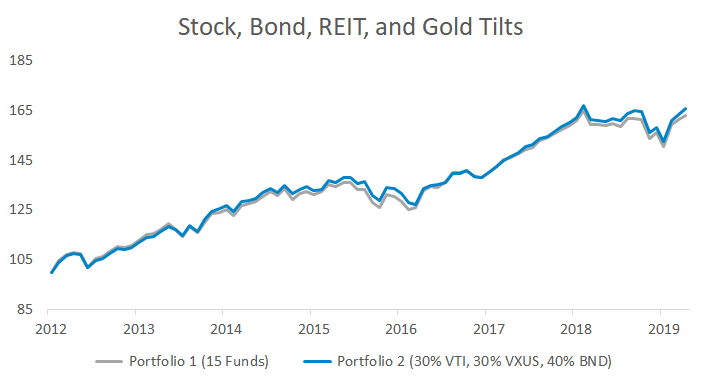

Ultimate Slice-and-Dice

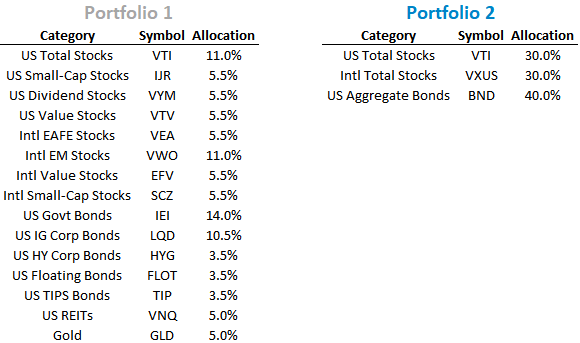

This final scenario splits stock, bond, REIT, and gold exposure across fifteen funds. A lot is going on under the hood – but have the returns been different than a simpler (and lower fee) solution?

Summary

There are two takeaways of the above data:

- Small portfolio changes don’t matter. Investors should either go all-in with substantially different allocations or simplify their portfolios.

- More funds doesn’t equal more diversification. Seeing 20 funds on a statement might make an investor feel more diversified, but ultimately it just creates unnecessary complexity.